Balanced Portfolio Recommendation: Trim 1/3 (take profit) Northern Star (NST)

You are unauthorized to view this page. Username Password Remember Me Forgot Password

Skip to content

Skip to content You are unauthorized to view this page. Username Password Remember Me Forgot Password

We recommend reallocating 2% of our portfolio from Elders (ELD) to Nufarm (GNC). This decision is based on the realization of a 9.2% profit in Elders and the assessment that Nufarm is currently undervalued, as supported by its recent earnings report and market conditions.

Overall, Challenger’s financial results for FY2024 appear to have exceeded market expectations, particularly in terms of profitability and EPS growth, despite slightly lower total Life sales. The company’s performance has been recognized by an increased dividend and a positive outlook from most analysts.

ResMed Inc.(RMD) pioneer innovative solutions that treat and keep people out of the hospital, empowering them to live healthier, higher-quality lives. Our digital health technologies and cloud-connected medical devices transform care for people with sleep apnea, COPD, and other chronic diseases. and lower costs for consumers and healthcare systems in more than 140 countries.

ADD to Challenger (CGF) into Earnings on the 13th August

Balanced Portfolio – SELL 5% Resmed (RMD) Take +10% profit

We recommended buying ResMed Inc. (RMD) due to its potential for strong performance in the upcoming earnings season on the 29th of July

ResMed Inc.(RMD) pioneer innovative solutions that treat and keep people out of the hospital, empowering them to live healthier, higher-quality lives. Our digital health technologies and cloud-connected medical devices transform care for people with sleep apnea, COPD, and other chronic diseases. and lower costs for consumers and healthcare systems in more than 140 countries.

Northern Star Resources, one of the largest gold producers, operates major mines in Australia and Alaska. Despite its solid operations and strong cash generation, NSR is currently undervalued compared to its peers. This undervaluation, coupled with its ongoing growth plans, makes it an attractive investment.

Overall, BHP has shown strong operational performance with record production in several key commodities and has met or exceeded its production and cost guidance for FY24. The company is actively progressing its growth and decarbonisation strategies, despite challenges in the nickel market.

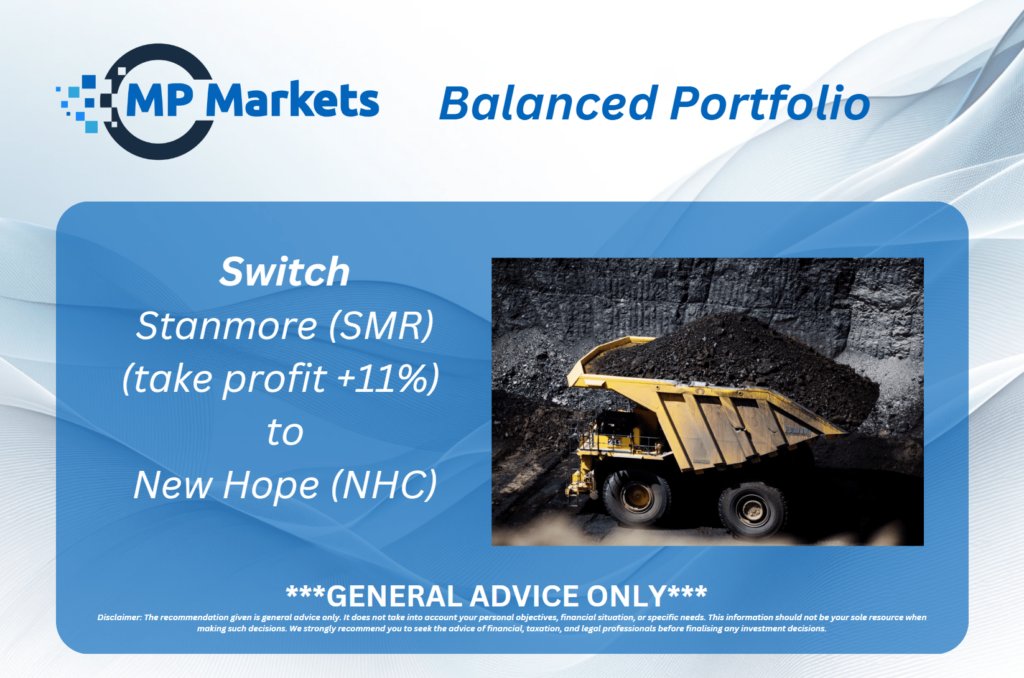

NHC is currently trading at a discount relative to its intrinsic value and peers, presenting an attractive entry point based on key valuation metrics.

Given the recent rally in Stanmore Resources Limited’s stock price, driven by the fire at Anglo American’s Grosvenor mine which significantly reduced global seaborne coking coal supply, we recommend taking profit on half of our position.

Optimized by Seraphinite Accelerator

Optimized by Seraphinite Accelerator