In the fast-growing world of artificial intelligence (AI), specialised hardware known as chips plays a central role, powering applications from chatbots to self-driving cars. For investors, understanding the differences between training chips and inference chips is essential, as they form distinct AI market segments with unique growth prospects. Training chips construct AI models, while inference chips apply them in practical settings. This article examines these differences, their applications, leading firms, and why traditional central processing units (CPUs) and random-access memory (RAM) are inadequate for large language models (LLMs), underscoring the demand for specialised hardware.

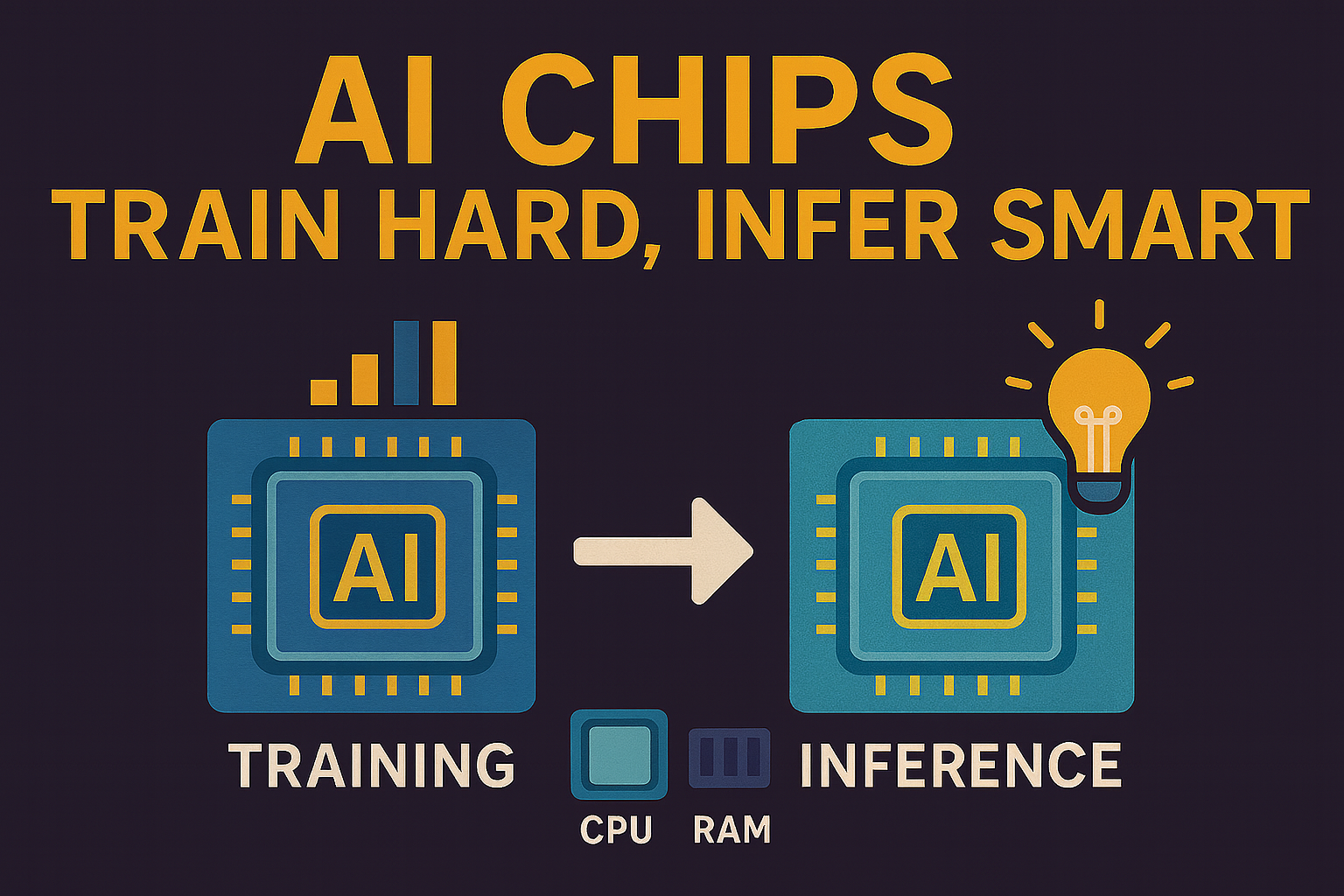

What Are Training Chips and How Are They Used?

Training chips drive AI development by processing vast datasets to teach models. They handle iterative calculations on billions of data points—like images or text—to refine parameters for accuracy. This intensive process demands massive power in data centres and can span weeks.

Tech giants and startups use them to build LLMs, such as those behind ChatGPT, for applications like healthcare drug discovery or finance fraud detection. Demand grows with advanced models, fuelling market expansion.

Key players: NVIDIA dominates with Blackwell GPUs and over 80% market share. AMD challenges via MI series and acquisitions; Google’s Alphabet leads with TPUs for internal training; Intel offers open-source Gaudi chips; Cerebras provides wafer-scale innovations. NVIDIA’s software ecosystem gives it an edge, but rivals offer cost-effective alternatives.

What Are Inference Chips and How Are They Used?

Inference chips apply trained models to new data, generating outputs like e-commerce recommendations or medical analyses. They prioritise speed, efficiency, and low power for real-time use on devices or servers.

These enable broad AI adoption in smartphone assistants, edge monitoring, and cloud analysis. Inference is more scalable than training, with repeated model deployment driving larger markets.

Leaders: NVIDIA extends dominance with L4 chips; Groq focuses on ultra-fast responses; Qualcomm excels in mobile via Snapdragon; Google uses TPU variants for cloud; Intel and AMD provide versatility. Startups like Mythic and Lightmatter innovate in efficiency.

Key Differences Between Training and Inference Chips

Training handles heavy, precise computations for learning, needing vast memory and power for data centres. Inference focuses on quick, low-energy operations with reduced precision for devices.

Training handles heavy, precise computations for learning, needing vast memory and power for data centres. Inference focuses on quick, low-energy operations with reduced precision for devices.

Chip types: GPUs (NVIDIA, AMD) are versatile but power-hungry; TPUs (Google) optimise tensor maths; NPUs (Apple, Qualcomm) offer low-latency for smartphones. Training sparks innovation; inference sustains revenue.

Why CPUs and RAM Are Not Effective for Processing LLM Models

Standard CPUs and RAM struggle with LLMs’ billions of parameters and parallel demands.

- Limited Parallelism in CPUs: Few cores (4-64) suit sequential tasks, not thousands of simultaneous operations like matrix multiplications, slowing AI processes.

- Poor Memory Bandwidth in RAM: Lacks speed for 100GB+ models; causes bottlenecks and delays.

- Energy and Cost Inefficiency: Excessive power use without optimisations; specialised chips deliver 10-100x better performance via high-bandwidth memory and parallelism.

Key Players in AI Chips

The AI chip market blends training and inference due to significant overlap many chips and companies serve both, with versatile designs handling heavy data centre workloads for model building (training) and efficient, real-time deployment (inference). NVIDIA dominates overall, but competition is heating up from tech giants, cloud providers, and startups focusing on cost, power efficiency, and specialisation. Foundries like TSMC and Samsung support production across the board.

- NVIDIA: Market leader with over 80% share; Blackwell GPUs excel in training, while L4 series leads inference revenue; CUDA ecosystem locks in users for both.

- AMD: Strong rival in training and inference via MI series; acquisitions like Untether AI’s team boost energy-efficient options for data centres and edge.

- Google (Alphabet): TPUs optimised for in-house training and cloud inference, offering high efficiency for large-scale AI tasks.

- Intel (Habana Labs): Gaudi chips compete in both segments with open-source focus; supports enterprise training and ecosystem-backed inference.

- Qualcomm: Entering aggressively with AI200/AI250 chips for data centre training/inference and mobile edge, challenging NVIDIA and AMD directly.

- Startups: Groq specialises in ultra-fast inference; Cerebras offers wafer-scale for massive training models; Mythic, Tenstorrent, Untether AI, and Lightmatter innovate low-power, efficient designs across both.

- Cloud Giants: Amazon (Trainium for training, Inferentia for inference) and Microsoft develop custom chips to enhance their AI services.

- Foundries (Production Support): TSMC leads advanced manufacturing; Samsung key for supply chain reliability.